Tax Pro Plus

2999 Overland Ave.

Suite 204

Los Angeles, CA 90064

Map It!

Ph: (310) 827-4829

Fax: (310) 842-7160

info@taxproplus-la.com

Better to Sell or Trade a Business Vehicle?

Article Highlights:

- Trade-in

- Sale

- Personal Use Allocation

- Other Considerations

Thus, it is generally better to trade in a vehicle that would result in a gain if it were sold and to sell a vehicle if doing so would result in a loss.

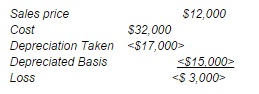

Let’s say a taxpayer sells a 100%-business-use vehicle for $12,000. The original purchase price was $32,000, and $17,000 is taken in depreciation. As illustrated below, the sale results in a loss, so it generally would be better to sell the vehicle and deduct the loss rather than trade in the vehicle.

If a vehicle is used for both business and personal purposes, the loss or gain must be prorated for the proportion of business use, as the personal portion of any loss is not deductible.

Since trade-in values are generally less than the sales value of the vehicle, the trade-in decision must also consider whether the tax benefits will exceed the additional money received from selling the old business vehicle. Of course, there is always the hassle of selling a car to be considered as well.

If you are considering trading a vehicle in, determine whether the tax benefits exceed the additional money received from selling the old business vehicle, as trade-in values are generally less than actual sales values. You should also consider the time and energy it will take to sell the vehicle on your own.

This concept can also be used when selling or disposing of other business assets. If you have questions about how this tax strategy might apply to your specific tax situation, please give this office a call.

The Tax Pro Plus newsletter is available via e-mail on a free subscription basis. You can subscribe or unsubscribe at any time. For more information about - Tax Pro Plus, go to http://www.taxproplus-la.com. This message was sent using ClientWhys Persyst. View our permission marketing policy.

Disclaimer: The tax advice included in this newsletter is an overview of some complex tax rules and is not intended as a thorough in-depth analysis of the tax issues discussed. Do not act on the information included in this newsletter without first determining how these issues apply to your particular set of circumstances and if there are any special tax laws or regulations that might apply to your situation.

|

|  |